If a country had the most-restrictive regulations on foreign direct investment (FDI) of 55 nations studied, where do you think it would rank among those nations in terms of actually attracting investment from abroad?

If you said “First,” you obviously would be flaunting conventional economic theory and engaging in highly counter-intuitive speculation. Further, you would be absolutely correct.

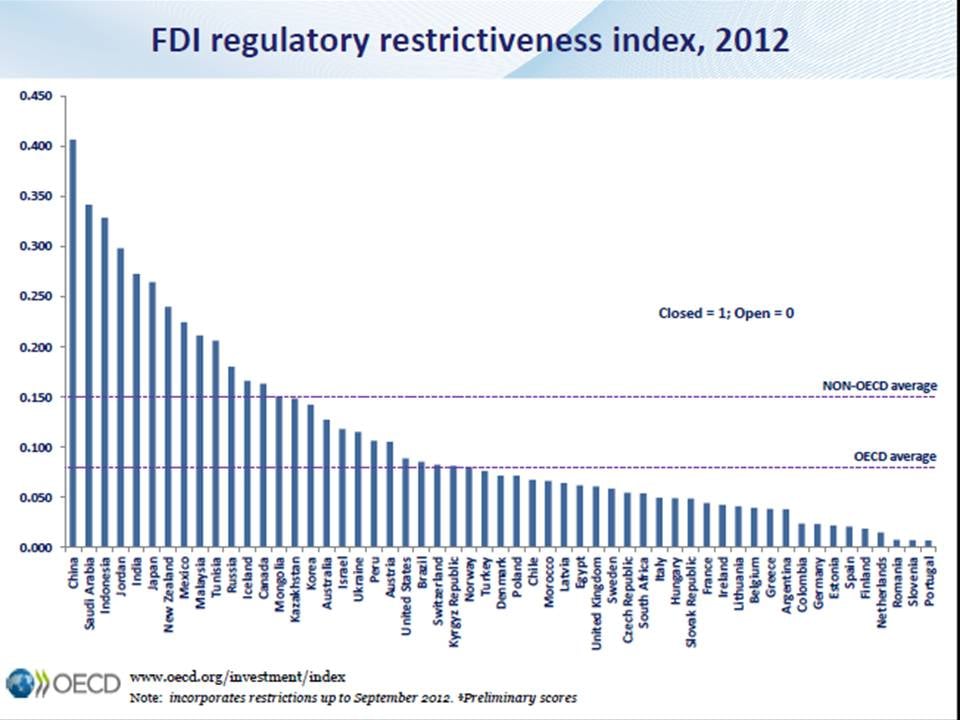

The Organisation for Economic Co-operation and Development (OECD) employs an “FDI regulatory restrictiveness index” to assess the extent to which countries regulate investment from outside their borders. Formulated in 2003, the index examines four types of restrictions – sectoral equity limits; screening; restrictions on key personnel, such as managers and directors; and other restrictions, such as those pertaining to capital repatriation, land, reciprocity, and similar factors. A score of 0 indicates an open economy, while a score of 1 signifies that the economy is closed.

The People’s Republic of China earned a score just above 0.4 in the latest iteration of the index. As the chart above shows, this gives China the dubious distinction of being first – or most restrictive – of the 34 OECD member nations and 21 other economies included in the 2012 index.

That wasn’t the only FDI-related gold medal China earned last year, however. According to the OECD, 2012 also saw the PRC surpass the United States as the world’s primary recipient of foreign direct investment. Even more impressive, this first-place standing was achieved against the backdrop of a significant worldwide decline in FDI relative to 2011.

The actual FDI numbers depend on which definition one uses, as explained in an excellent blog post by the Rhodium Group’s Thilo Hanemann, but the figures are impressive regardless of the preferred approach for calculating them. Preliminary estimates released by the OECD this spring showed the PRC enjoying FDI inflows of $253 billion last year, or 18 percent of the global total. This figure is in line with the fairly broad definition of FDI employed by the People’s Bank of China and its State Administration for Foreign Exchange (SAFE). Meanwhile, the United Nations Conference on Trade and Development, or UNCTAD, using a narrower definition in line with calculations employed by Beijing’s Ministry of Commerce, puts FDI inflows to China at $119.7 billion for 2012. (Unlike the OECD, UNCTAD puts the U.S. in first place for 2012, at $146.7 billion, although calculating that US inflows of FDI declined by 35 percent from 2011, compared with a drop of just 3.4 percent for China.)

What’s more, recent concerns about slowing growth haven’t diminished the luster that China holds for the world’s investors. Figures released last week by the Ministry of Commerce show that China attracted $71.4 billion in FDI from January through July, up more than 7 percent from the same period last year.

In a further rebuff to the conventional wisdom, the countries ranked by the OECD as having the second and third most-restrictive regulatory environments for FDI also significantly outperformed the global average in attracting outside investment last year. Saudi Arabia, the runner-up, saw its 2012 FDI inflows grow by 15 percent relative to 2011, according to the OECD, while third-place Indonesia held steady from one year to the next at $19.2 billion.

And what rewards were reaped by the country deemed by the OECD to be most open to foreign investment? Given the economic woes of the Iberian Peninsula, teasing out the impact of one factor in the overall mix is particularly difficult in this case, but after seeing its FDI inflows quadruple from 2010 to 2011, Portugal experienced an 11.8 percent decline in FDI in 2012 to just $9.2 billion.

So, what can we learn from contrasting the FDI restrictiveness and attractiveness of polar opposites China and Portugal? There are two, inter-related lessons to be drawn. First, size matters. The prospect of doing business in a country of 1.3 billion people makes restrictions that might be deemed intolerable elsewhere somehow manageable. Second, while a regulatory environment favorable to investment almost certainly does give a country a competitive advantage “all else being equal,” per the ceteris paribus models that economists love to construct, in the real world all else isn’t equal, and those inequalities often make all the difference.