(L to R) Presidents from Bolivia, Evo Morales, Uruguay, Jose Mujica, Brazil, Dilma Rousseff, Argentinian Cristina Fernandez de Kirchner and Ecuador, Rafael Correa, pose for the official picture of the Summit of Heads of State of Mercosur and Associated States, at Itamaraty Palace, Brasília on December 7, 2012. (Credit: PEDRO LADEIRA/AFP/Getty Images)

Latin America will suffer a recession this year. According to the IMF, regional GDP will contract by 0.3% in 2016. This will not only have economic consequences for the next three years, but also transform Latin American politics, ending a decade-long division.

This division was more evident after 2012, when Venezuela joined Mercosur, creating a common block of Mercosur and the Bolivarian Alliance (ALBA)—to be fair, Uruguay and Paraguay were trapped in between. Argentina, Bolivia, Brazil, Cuba, Ecuador, Nicaragua and Venezuela embodied the left: growth model based on public expenditure financed by the commodity boom; dependency on China; and explicit rejection of forming closer ties with the United States.

A group Central American and the Pacific-Alliance countries stood out in contrast: Chile, Colombia, Peru and Mexico. These countries were governed by center-right parties, had a growth model more dependent on free trade and less so on public expenditure and had closer ties with the U.S.

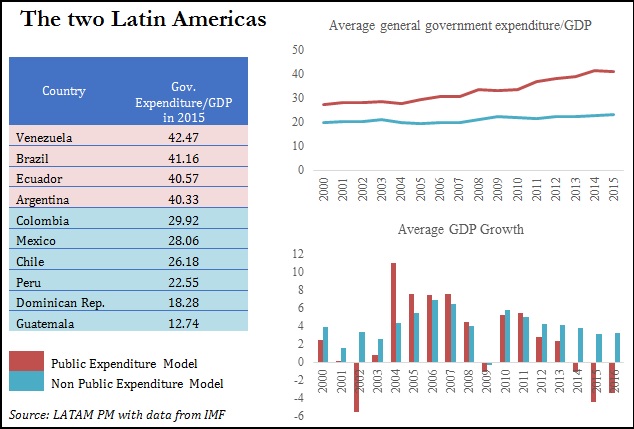

To better illustrate this point, take the 10 largest economies in the region and list them by the level of government expenditure relative to GDP. A clear division is evident. Filtering for the countries with a ratio above 40% can yield interesting patterns. The level of government expenditure was already higher for this group of countries in 2000, but it increased significantly after the financial crisis of 2008 and slowed down after 2014. In terms of growth, after Argentina and Brazil overcame their crises in the early 2000s, this group grew at a faster pace. However in 2009 and 2014-16, they have experience economic downturns.

So what? The region as a whole will experience important challenges: lower fiscal revenue, capital flight, depreciating currencies, weaker demand for exports, etc. The difference is that Argentina, Brazil, Ecuador and Venezuela will have to go through a more painful process that will bring political change. Since those governments are moved by a strong ideology, they are unwilling to undergo reforms to their economic models.

This has already started. In Brazil, Dilma Rousseff leftist Worker’s Party (PT) almost lost the presidential election in a runoff against Aécio Neves, the center-right PSDB candidate, in October 2014. Since then, things have been chaotic for Dilma and the PT. Currently, the shadow of a possible impeachment follows the president. While the possibility of an actual impeachment is low, its sole presence has contaminated Brazilian politics, draining important energy and time from policymakers.

Key policy changes to revive much-needed economic growth are hampered, together with the chances of the PT maintaining its hold on power in the next election cycle. As unemployment and inflation keep rising, the possibility of a turbulent transition increases. The World Cup triggered important social instability in 2014, as the contrast between the government’s frivolous spending in the event and the dreadful state of public services enraged the public. The upcoming 2016 Olympics in Rio de Janeiro might be yet another trigger.

In Argentina, the political transition has already materialized. Cristina Fernandez was not as lucky as Rousseff, and her fellow Peronist appointee, Daniel Scioli, lost to center-right Mauricio Macri in November’s presidential election runoff. Since Macri took office earlier this year, a lot has changed. He lowered tariffs and taxes on exports, removed capital controls and let the peso float freely. He announced cuts in subsidies and new negotiations with U.S. hedge funds, too.

Perhaps more importantly for the region, Macri affirmed that he wants Venezuela out of the Mercosur and that Argentina wishes to join the Pacific Alliance. Still, Macri has an uphill battle ahead; he will have to face a hostile congress—controlled by Fernandez’s party—that resumes activities in March, as well as deep economic imbalances. Inflation is one example. Macri wants to bring down inflation to 25% in 2016, although this is seen as too optimistic by market participants.

Maduro and the PSUV have not only lost an important ally with Macri’s victory. In Venezuela, the PSUV, the party founded by Hugo Chavez, lost the elections for the National Assembly by a landslide. The opposition now controls 2/3 of the legislative and has threatened to call a referendum this year to remove Maduro from power. Although the PSUV still maintains control over several key institutions, such as the Supreme Court, one thing is certain: transition has started. As in the Brazilian case, as the economic situation worsens—from an already disastrous 10% GDP plunge in 2015 and 300% annual inflation—the risk for an abrupt and more violent transition increases.

Ecuador is not in a situation as critical as its peers. True, it is going through a hefty fiscal consolidation and growth fell from 4% in 2014 to 0% last year. The government is expecting 1% growth in 2016, but even the IMF’s 0.05% forecasts looks too optimistic given the 12% government budget cut in a country so dependent on public spending for growth. Moreover, the government’s forecast for this year assumed an oil price of $35 per barrel. (Oil a significant source of fiscal and current account revenues.) The Ecuadorian oil mix reached $20.7 per barrel on January 19 and president Correa acknowledged that the country is already pumping oil at a loss—production cost is $24 per barrel.

Despite his 60% approval rate, Correa was not able to prevent large street protests last year. He even had to retract some unpopular law initiatives and announced that he is not running in 2017 in order to gain enough political capital to pass an amendment that eliminates the presidential reelection limit. (LATAM PM analysts believes that he is trying to come back Putin-style in 2021, but that is a different story.) His strategy faces many risks.

The following years are going to be crucial in defining regional politics and international relations. It is important to recognize that the aforementioned countries have made important achievements in terms of economic development during the last decade. Millions were lifted out of poverty thanks to social programs financed by public spending. Still, it was shortsighted and risky to depend so much on China’s demand for commodities.

This article was originally published by LATAM PM and written by LATAM PM analyst Fernando Posadas.