Writing on Brazil has become an exercise in futility. With the ever-accelerating tempo of political developments, articles on the country’s political crisis must constantly be updated and predictions seem anachronistic within a week’s time.

To avoid the alluring trap of offering the most current state of affairs, I suggest instead taking a step back and looking at the big picture before diving into the mechanics of the impeachment and its possible consequences for the future of Brazil. I will thus refrain from discussing the ongoing investigation around ex-president Lula and his recent ministerial nomination as Dilma’s Chief of Staff.

Back in the summer of 2013, there were already indications of the country’s deep malaise. This was expressed by the largest street protests at the time (the latest pro-impeachment protests on March 13th have shattered that record, bringing around 1.5 million people to the streets of São Paulo alone and 3.6 million nationwide) since 1992, when Brazilians took to the streets to demand the impeachment of president Collor over corruption charges.

Then, the economy was showing early signs of decline, with GDP growth slowing down to a halt while government spending kept on rising, especially in the run-up to the October 2014 election (the deficit that year doubled to 6.75% of GDP).

By the time Dilma guaranteed her second presidential term in a tight race (she won 51.59% of the vote), a federal police investigation—dubbed Operation Car Wash—started to grab the headlines. Quickly, what began as a money laundering investigation grew exponentially to encompass corruption allegations at the state-controlled oil company Petrobras. This is when all hell broke loose.

A corruption scheme—the Petrolão—in which Petrobras suppliers and subcontractors bribed the firm’s executives in return for inflated contracts, was unveiled. As investigators dug deeper, they found that a percentage of the contracts’ value were diverted into slush funds for political parties, thus implicating politicians in the ruling coalition led by Dilma’s Working Party (PT).

The biggest corruption scandal in Brazilian history dealt a severe blow to the PT’s image, bringing Dilma’s approval ratings down into the single digits and shattering investor confidence. By then, the nascent political crisis was compounded by an increasingly visible and painful economic slowdown.

The latest twist to the investigation came on March 22nd 2016 with Marcelo Odebrecht’s decision to accept a plea-bargaining deal. The former chief executive of Latin America’s largest construction company, Odebrecht SA, had received a 19-year sentence for bribery, money laundering, and organized crime related to the corruption scandal. Spreadsheets released to the press reveal over 200 names of politicians involved in the corruption scheme, among them Aécio Neves the center-right candidate in the 2014 elections, Rio de Janeiro’s mayor Eduardo Paes, Rio’s governor Luiz Fernando Pezão, and the president of the Chamber of Deputies Eduardo Cunha among others.

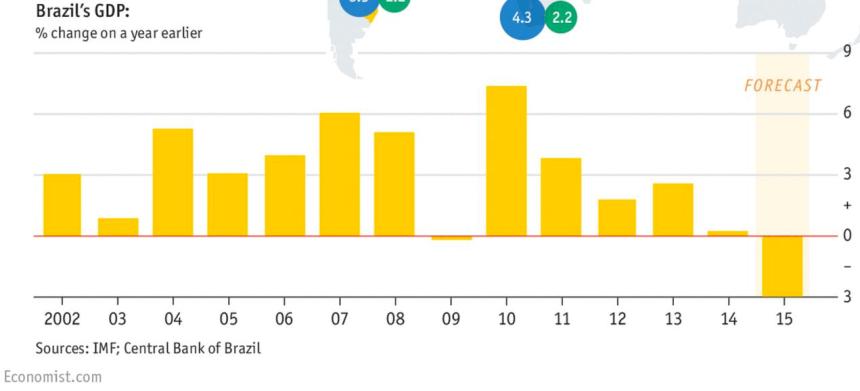

Brazil’s economic “boom” (2004-2013)—driven by unsustainable consumption, fast credit expansion and China’s never-ending appetite for Brazil’s commodity exports—peaked in 2010 when the country grew by 7.5% and helped lift some 40 million out of extreme poverty in a country of 203 million.

However, as China started to slowdown, dramatically decreasing its imports from Brazil, and the price of oil collapsed, old problems are resurfacing. Obstacles to operating Brazil are so perennial in nature that they have simply been nicknamed “Custo Brasil”—a combination of a high tax rate (36% of GDP), a byzantine tax system, poor infrastructure leading to bottlenecks, and high labor costs combined to outdated labor laws.

In addition, Dilma’s government fiscal imbalance has become a problem after years of fiscal irresponsibility. Since 1988, the constitution enshrines about 90% of expenditures as mandatory spending linked to growth and inflation. With the government revenues dramatically decreased, deficit has crept to about 10% of GDP with little room for an adjustment.

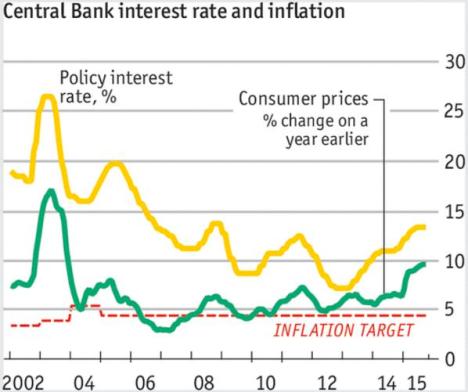

Such a large deficit is creating a problem of fiscal dominance in which the central bank is incapable of reining in inflation (at 10.67% for 2015) through interest rate hikes (already at 14.25%). In such a scenario, due to questioning over debt stability, rising interest rates would lead to currency depreciation and an increase in inflation instead of a fall. Price levels are then determined by fiscal policy rather than monetary policy.

(The Economist)

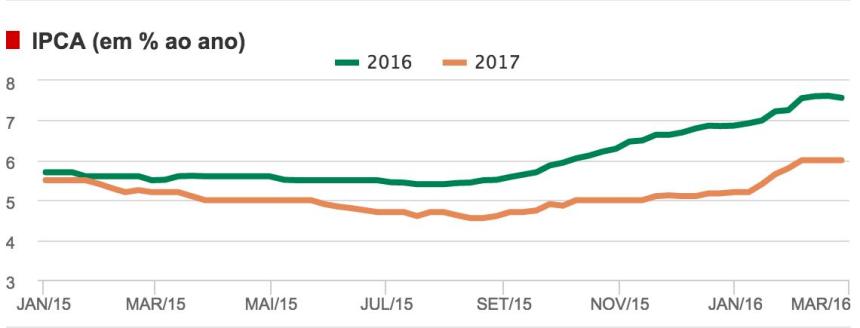

To give a better sense of the dramatic situation Brazil finds itself today, here are a couple key economic indicators. Brazil’s GDP contracted by 3.5% in 2015 and the recession is expected to continue unabated throughout 2016, with the central bank predicting another contraction of 3.6% for this year and growth only timidly returning in 2017 at 0.44%. In 2015, annual inflation closed at 10.67%. This year it is predicted to fall slightly to 7.5% and to around 6% for 2017.

(Valor Economico)

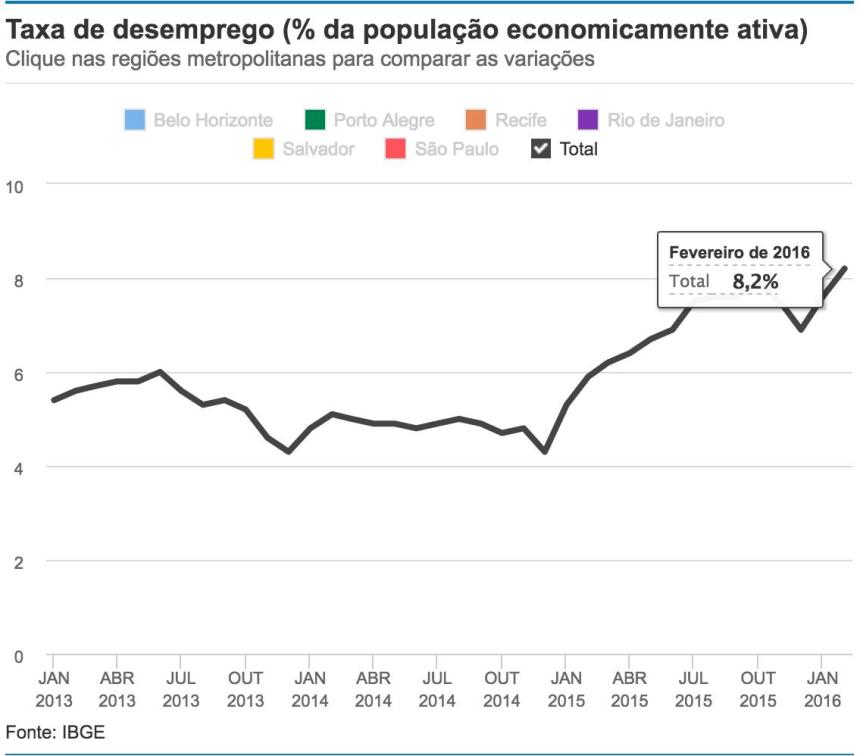

For a while, although growth was weak, unemployment remained close to record lows. This lasted until January 2015. In one year, the unemployment rate skyrocketed from 5.3% to 7.6% of the labor force in January 2016. The latest estimate for February is of 8.2% for the country as a whole, but reaching up to 12.6% in cities like Salvador. In absolute terms, over 2 million Brazilians are now unemployed, further straining the government’s already shaky finances.

(Valor Economico)

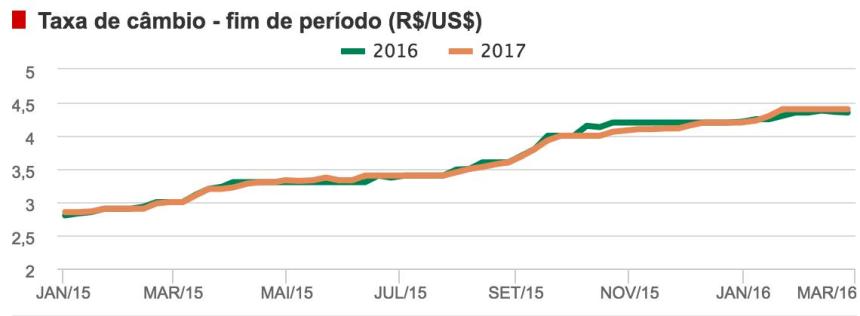

On the positive side, the real/U.S. dollar exchange rate has fallen dramatically to 3.59 R$/USD, influenced by the current political environment, as a possible impeachment of president Dilma becomes ever more likely. The Bovespa stock exchange has experienced a similar resurgence, growing by 16.15% this month. But market optimism will probably be short-lived as the necessary structural reforms are as unlikely to be passed whether Dilma Rousseff or her vice president Michel Temer are in power. This sober perspective is confirmed by predicted exchange rates of around 4.5 R$/USD for the end of 2016 and 2017.

(Valor Economico)

Many pundits talk about the likelihood of Dilma’s impeachment but fail to explain the motive, its mechanics and the successive stages leading to her removal from office.

(Estadão)

The first step occurred on March 17th, when the Chamber of Deputies, after the decision of Eduardo Cunha, elected a 65-member special commission to analyze the impeachment request of President Dilma Rousseff. The commission is composed of members of all parties, allocated proportionally to their number of seats in the lower house. She stands accused of accounting trickery to mask the size of the government budget deficit. In actuality, she is paying for her mismanagement of the economy and suffering from the blowback of the corruption scandal, which turned popular opinion overwhelmingly against her.

Once the commission is installed, Dilma has ten plenary sessions of the chamber to present her defense against accusations. The collegiate has the five subsequent plenary sessions to vote on whether or not to continue the impeachment process. The Chamber’s president, Eduardo Cunha, has vowed to hold sessions every working day of the week, in an attempt to speed up the procedure. To count, each session must have at least 51 out of the 513 deputies present.

Within 48 hours of the commission’s vote, its recommendation is included in the agenda of the next plenary session. During the session, the impeachment motion is opened if at least 342 of the 513 deputies vote in favor.

Once the impeachment motion is opened, it moves up to the Senate to be analyzed. Presided by the president of the Supreme Court, the session will decide on the impeachment. If approved by a simple majority (1/2+1, that is 41 of the 81 senators), Dilma is removed for up to 180 days until the final decision is taken while her vice-president Michel Temer takes her place temporarily. Finally, if 2/3 of the Senate subsequently approves the impeachment (54 of the 81 senators), Dilma is permanently removed and Michel Temer assumes office until the rest of term in 2018. Otherwise, she reassumes her mandate immediately.

Polls conducted by Arko Advice with 100 deputies of 23 parties between March 15th and 17th find that 62% believe that the Chamber will approve the impeachment. In February, the percentage was only 24.5%, tripling in only three weeks. The percentage of those who thought the impeachment would be rejected fell from 66.66% to 27% in the same period. Thus, there is a significant possibility that the motion will pass on to the Senate. However, once in the Senate—where Dilma enjoys significant more support than in the lower chamber—the process will be delayed but eventually passing. Indeed, it will be hard for senators to go against the Chambers’ vote and popular sentiment (68% of Brazilians are currently in favor of impeachment).

Nevertheless, even if Dilma is impeached with Temer assuming the presidential office, this is no panacea to Brazil’s troubles. With only two years left in the current electoral cycle and the PMDB’s interest in fielding its own candidate in the next presidential elections, it is unlikely that the painful fiscal readjustment and unpopular structural reforms that need to be implement in order to put the country back in track would be carried out by a Temer government. Moreover, much of Brazil’s economic woes can be attributed to the negative external economic environment that gives no signs of improvement in the near future.

In the short-term Brazil will remain in a critical economic situation—at least until 2018. In the long-term, the current crisis demonstrated the institutional resilience of the Brazilian democracy and the engagement of its new middle-class, while exposing the country’s dependence on commodity exports and household consumption and the need to diversify its economy. Beyond the long storm, the future looks bright.

This article was originally published by LatAm PM.