The Fed, Trade, and Dollar Purchasing Power

By Robert Elway

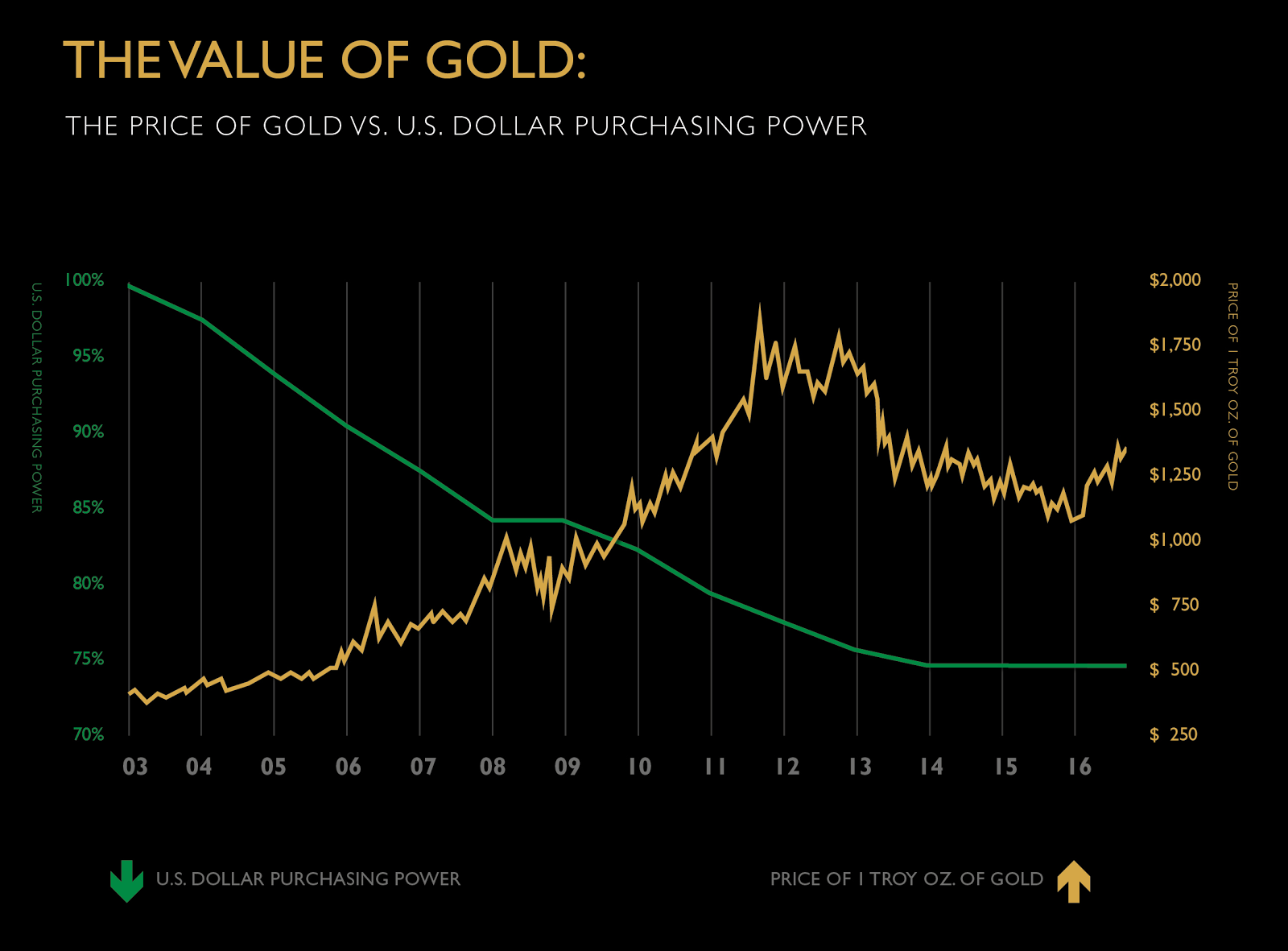

Study the US economy and its relationship to other countries and you will see two effects of the Federal Reserve’s accommodative monetary policy: higher gold and lower US dollar purchasing power.

From January 2003 to March 2017, the Effective Federal Funds Rate (EFFR) dropped by 36% while gold rose 169%, and dollar purchasing power reflects this low-rate environment. One 2017 dollar equals only seventy-five cents in 2003 dollars. The US dollar has remained at 75% purchasing power since 2014, making the nominal prices of goods and services more expensive in the United States than they were fourteen years ago.

The Fed’s Impact on International Trade

From the perspective of the US, the trade balance increased in 2009 and has remained above 2004-2008 averages since then. Our trade gap with China has gotten larger since 2012, mainly by rises in imports of consumer goods.

At least for a time of mass appeal among American consumers, platform-based products like the iPhone can create more production in goods and services than the sum of their parts. In addition to the suppliers of the physical goods used in manufacturing the phone, there is also the platform it creates for an increasingly services-oriented environment indirectly fueled by easy money from central banks around the world.

Especially in a low interest rate environment as the US has been experiencing since 2009, importing some goods can create growth in domestic industries like technology-based services.

The Fed’s accommodative policies have led to a paucity of traditional returns from US government bonds, which tends to make venture capital and other, often riskier, forms of investing more attractive to the traditionally risk-averse. This leads to pension funds investing in venture capital firms which fund startups that support New Economy jobs.

We’ve heard news stories about these jobs, especially with Uber and other apps-turned-employers in the United States–all created, or in the very least facilitated, by a platform that takes advantage of the Chinese-manufactured iPhone and an ever-larger amount of capital looking for above-average return.

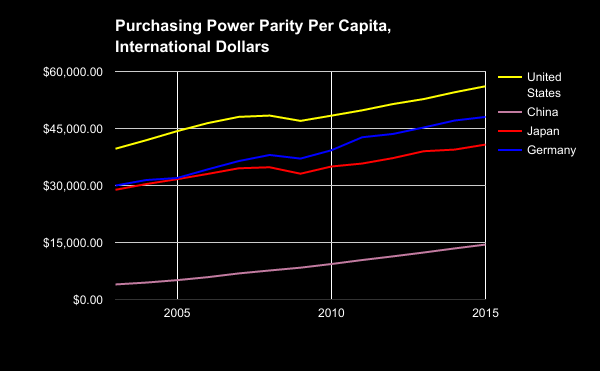

Purchasing Power Parity (PPP) controls for nominal price disparities that result in nations having a different cost of living, allowing for economists to compare multiple countries’ output, usually expressed in terms of International Dollars. This is a unit of currency based on the US dollar’s purchasing power during a specific year that is kept consistent throughout the comparison with other countries.

For the example below, purchasing power parity can be derived from GDP or by equating the Consumer Price Indices of individual countries. The PPP exchange rate determines how many US dollars, Chinese yuan, Japanese yen, or euros consumers in their home countries would need to convert to International Dollars in order to equal the same purchasing power as consumers in other countries for a given year.

Using 2017 as a reference year for per capita PPP produces Charts 1 and 2 below.

Chart 1: Higher PPP

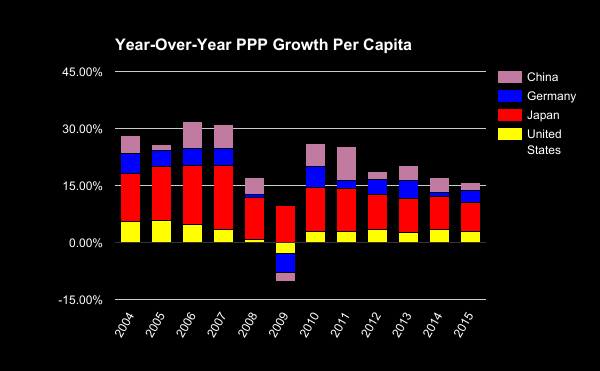

Chart 2: Lower PPP Growth

Back in 2006 and 2007, Chart 2 shows that total PPP per capita for the US, Germany, Japan and China was growing over 30%. In 2009, China, Germany and the US all had decelerating growth while purchasing power parity still grew in Japan. However, Japan’s shrinkage in growth from 2010-2015 had the greatest impact on the overall total. While the pre-financial collapse years saw over-15% growth just from the US and Japan alone, all four countries’ PPP growth barely amounted to this same benchmark by 2015.

Robert Elway is a financial analyst at Rosland Capital, a precious metals company that tracks gold pricing, monetary policy and other financial news.